Most startup advice treats fundraising and bootstrapping as opposing choices. You either raise venture capital and grow fast, or you bootstrap and grow slow. That framing has always been too simple, and in 2025 it is increasingly out of step with how the most thoughtful founders are actually building companies.

The startup booted fundraising strategy sits between those two poles. It is not about refusing external capital or chasing it. It is about sequencing. It is about building enough real traction on your own resources that when you do approach investors or lenders or grant committees, you are not asking them to take a leap of faith. You are showing them a business that is already working and asking them to pour fuel on a fire that is already lit.

According to PitchBook’s Q3 2025 Venture Monitor, the share of sub-five-million-dollar funding rounds fell to its lowest level in a decade, at just over 50 percent of all VC deals. That contraction is pushing more early-stage founders toward self-funded growth, and it is revealing something that was always true but easier to ignore during the easy-money years: companies that arrive at fundraising conversations with revenue, customers, and operating discipline consistently raise at better valuations, on better terms, and with more leverage than those who arrive with only an idea and a pitch deck.

This guide is for founders who are building that foundation. It covers what the booted fundraising strategy actually means in practice, the specific capital sources available to self-funded startups, the sequencing decisions that determine when and how to raise, and the mistakes that cost founders equity and control before they have had a chance to build either.

Contents

- 1 What the Startup Booted Fundraising Strategy Actually Means

- 2 The Funding Landscape in 2025 and Why This Strategy Is More Relevant Than Ever

- 3 Phase One: Building the Foundation Before Any Fundraising Conversation

- 4 The Capital Sources Available to Booted Startups

- 5 When to Transition from Bootstrapping to Active Fundraising

- 6 Bootstrapped vs VC-Backed vs Booted: A Practical Comparison

- 7 What the Founders Who Got This Right Actually Did

- 8 The Psychological Traps That Derail Booted Fundraising Strategies

- 9 Mistakes That Cost Booted Founders Equity and Opportunity

- 10 Frequently Asked Questions

- 11 Conclusion

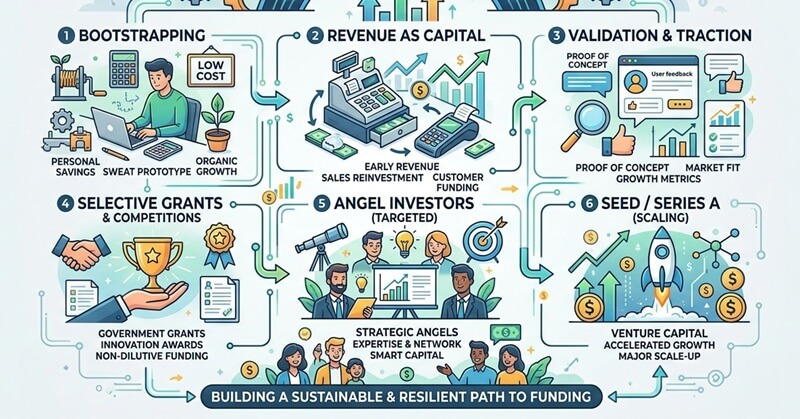

What the Startup Booted Fundraising Strategy Actually Means

The term gets used loosely, so it is worth being precise. A startup booted fundraising strategy is a capital-raising approach where founders deliberately build traction using their own resources before seeking external funding. The core principle is that you raise capital to accelerate momentum, not to create it.

This is different from pure bootstrapping, which means building an entire business without external investment and often implies a deliberate commitment to staying independent. The booted strategy does not foreclose external capital. It changes the timing and the terms under which that capital enters. You bootstrap through the messy early phase, develop a product that paying customers actually use, build a revenue base however modest, and then approach fundraising from a position of demonstrated value rather than projected potential.

The difference in outcome is significant. A founder raising at the idea stage with no customers typically gives away 20 to 30 percent of the company for a seed round. A founder raising with 18 months of operating history, a handful of paying customers, and measurable month-over-month revenue growth often raises the same amount of capital for 10 to 15 percent dilution. The money is identical. The equity given up is not. That gap, compounded across multiple rounds, is the difference between a founder who owns a majority of a successful exit and one who does not.

It is also worth saying what the booted fundraising strategy is not. It is not the right approach for every startup. Hardware companies, biotech, deep tech, and any business that requires significant capital expenditure before it can generate a single dollar of revenue often cannot bootstrap through early development. The strategy is most powerful for software companies, professional services, consulting, content businesses, and marketplaces where early revenue is achievable with minimal infrastructure. For those businesses, it is among the most founder-friendly approaches available.

The Funding Landscape in 2025 and Why This Strategy Is More Relevant Than Ever

The venture capital market that dominated startup culture from 2010 through 2021 was an anomaly. Interest rates near zero made institutional capital cheap and abundant, which flowed into early-stage startups on terms that were historically unusual. Valuations were high, due diligence was light, and the availability of follow-on funding created a safety net that encouraged founders to raise aggressively and burn quickly.

That environment is gone. Interest rates rose sharply from 2022 onward. The cost of capital increased. LPs became more selective about the funds they backed. Venture firms became more selective about the companies they funded. The era of pre-revenue unicorn valuations gave way to a return to fundamental metrics: revenue, retention, efficiency, and a clear path to profitability.

SaaS Capital’s 2025 research on bootstrapped companies with three to twenty million dollars in annual recurring revenue found that these companies maintain a median growth rate of approximately 20 percent annually while operating near breakeven or profitably. Equity-backed companies in the same revenue range showed a median growth rate of 25 percent, a meaningful difference in speed but one that comes at the cost of 15 to 40 percent equity dilution across multiple rounds. The question every founder must answer is whether that additional five percentage points of growth is worth what it costs in ownership and control.

For most startups in most markets, the honest answer in 2025 is no. The markets that genuinely reward blitz-scaling, those with strong winner-take-all network effects, massive distribution advantages, or fundamentally capital-intensive moats, are a small fraction of the startup universe. The rest are better served by the discipline that constrained resources create.

Phase One: Building the Foundation Before Any Fundraising Conversation

The first phase of a booted fundraising strategy is not about fundraising at all. It is about building the thing that makes fundraising possible on good terms. What that looks like in practice varies by business type, but the underlying goals are consistent: validate that someone will pay for what you are building, build a minimal version that actually delivers the promised value, and develop enough operating history to demonstrate that the business has legs.

Validate Before You Build

The most expensive mistake in early-stage startups is building something no one wants to pay for. The booted strategy forces this validation because you cannot fund your way past the problem. Without investor capital absorbing the cost of premature scaling, a product that does not generate revenue becomes a crisis rather than a runway extension.

Validation does not require a finished product. It requires evidence that someone will exchange money for the value you are proposing to deliver. This can mean a paid letter of intent from a potential customer, a refundable deposit, a consulting contract structured around the outcome your product will eventually automate, or a pre-sale campaign for a digital product. The form matters less than the signal. If no one will pay for it before it is built, that is information you need before you spend months or years building it.

The Revenue-First Operating Model

Once you have validated demand, the operating model during bootstrapped growth has one overriding priority: revenue per dollar spent. Every hiring decision, every tool purchased, every marketing channel tested should be evaluated against its contribution to bringing money into the business. This is not austerity for its own sake. It is the development of a discipline that makes you genuinely attractive to investors later, because it produces the efficiency metrics that sophisticated investors find most compelling.

Customer acquisition cost relative to lifetime value is the foundational metric of this phase. If you are spending more to acquire a customer than that customer will generate over their relationship with the business, no amount of fundraising fixes the problem. It only defers and amplifies it. Building a business where the unit economics are sound from the beginning is the most durable thing you can do with early-stage constraints.

Customer-Funded Development

One of the most underused funding mechanisms available to early-stage founders is the customer’s own willingness to pay in advance for a solution they need. This can take several forms. Charging a deposit on delivery several months out converts future revenue into present working capital. Offering an annual prepayment discount converts monthly subscribers into a lump-sum payment that funds the next development cycle. Negotiating non-recurring engineering fees for product customisation means a customer funds the development of a feature that then becomes part of the standard product.

These arrangements require a customer who trusts you enough to pay before the full solution exists. That trust is built through the quality of the relationship, the specificity of the solution you are proposing, and the credibility you have established through early interactions. It is not available to every startup at every stage. But for founders who have identified a specific, high-pain problem for a specific customer, it is often more accessible than they assume.

The Capital Sources Available to Booted Startups

One of the most persistent misconceptions about the booted fundraising strategy is that it means having no access to external capital. It does not. It means using external capital selectively and strategically, from sources that align with your stage, your business model, and your ownership goals. The following sources are available to founders at various stages of a bootstrapped trajectory.

Angel Investors

Angel investors are individuals who invest their personal capital in early-stage companies, typically in exchange for equity. Unlike venture capital firms, angels are not managing institutional money on behalf of limited partners, which means they are not bound by the same return timelines or growth expectations. A well-chosen angel investor brings not just capital but relevant industry relationships, hiring networks, and practical operator experience.

Founders using the booted strategy typically approach angels after they have initial revenue or a clear validated product, rather than at the idea stage. This positioning produces better outcomes in two ways. First, traction gives the founder genuine leverage in the negotiation. Second, angels who invest in companies with demonstrated traction are making a lower-risk bet, which often makes them more supportive and patient investors over the long term.

Revenue-Based Financing

Revenue-based financing is a form of capital where an investor provides an upfront sum in exchange for a percentage of monthly revenue until a predetermined repayment cap is reached. Unlike equity financing, it does not dilute ownership. Unlike debt, it does not require fixed repayments regardless of revenue performance. When revenue is low, repayments are low. When revenue grows, repayments accelerate.

This model works well for businesses with recurring revenue and predictable retention. SaaS companies with consistent monthly recurring revenue are well suited to revenue-based financing because the investor can underwrite the risk against an existing revenue stream rather than projected future growth. Providers like Clearco, Capchase, and Pipe offer variations of this model. The cost of capital is higher than traditional debt but the terms are more flexible and the founder retains full equity.

Non-Dilutive Grants

Government grants and innovation funding programmes represent a genuinely underused capital source for technology startups. The United States Small Business Innovation Research programme, known as SBIR, distributes over three billion dollars annually to small businesses conducting research and development. Phase one grants typically range from 50,000 to 275,000 dollars and require no equity and no repayment. Phase two grants can reach two million dollars.

Similar programmes exist at the state level and through industry-specific agencies. The National Institutes of Health, the Department of Energy, the Department of Defense, and the National Science Foundation all administer their own innovation grant programmes. European founders have access to Horizon Europe and national innovation funds. These programmes are time-consuming to apply for, which is exactly why most startups do not pursue them, and that low competition is part of what makes them valuable.

Startup Accelerators and Incubators

Accelerators like Y Combinator, Techstars, and hundreds of sector-specific programmes offer a combination of capital, mentorship, and network access in exchange for a small equity stake, typically ranging from five to ten percent. For founders pursuing a booted strategy, the right accelerator at the right moment can compress years of relationship-building into a few months while providing access to a pool of potential customers, advisors, and future investors.

The key consideration is timing. Entering an accelerator too early, before you have a clear product thesis and some evidence of demand, means you are spending equity on mentorship for problems you have not yet encountered. Entering with a working product, early customers, and a clear growth hypothesis means the programme accelerates something that already has momentum.

Selective Angel Rounds and SAFE Agreements

For founders who want to bring in some external capital without committing to a full priced equity round, a small angel round using a Simple Agreement for Future Equity, commonly called a SAFE, is often the right instrument. A SAFE converts to equity at a future priced round at a discount to whatever valuation that round establishes, with an optional valuation cap that protects early investors.

The advantage for the founder is speed and simplicity. A SAFE round can close in days rather than months. It does not require an agreed valuation at the time of investment, which reduces negotiation friction when the company is early and valuation is genuinely uncertain. The disadvantage is that the dilution is deferred rather than eliminated. SAFEs convert to equity, and founders who raise multiple SAFE rounds without a subsequent priced round can find themselves significantly more diluted than they expected.

Also read: Dealership Advertised Pricing Tactics Explained

When to Transition from Bootstrapping to Active Fundraising

Timing the transition from self-funded growth to external fundraising is one of the most consequential decisions a founder makes. Raising too early means giving up equity and control before the business has demonstrated enough value to command reasonable terms. Raising too late means potentially ceding ground to better-funded competitors or missing a market timing window that does not reopen.

The right time to raise external capital is not a date on a calendar. It is a set of conditions. The business should have paying customers with measurable retention, meaning customers who came back, upgraded, or referred others. The unit economics should be sound, meaning customer acquisition costs are lower than the value those customers generate. There should be a specific identified bottleneck, whether that is hiring, marketing spend, infrastructure, or inventory, that additional capital can demonstrably remove. And there should be evidence that removing that bottleneck would produce proportionally greater revenue, not just proportionally greater spending.

One useful test is to ask what you would do with the capital and why you cannot do it with revenue alone. If the answer is genuinely time-sensitive, if a market window is closing, a competitor is scaling fast, or a hiring opportunity is time-limited, then external capital may be the right accelerant. If the honest answer is that you want to grow faster without a specific, validated reason that speed matters, then the cost in equity and control is probably not worth it.

Founders who raise capital out of anxiety, because the bank balance is declining and the pressure is psychological rather than strategic, almost always raise on poor terms. Investors are skilled at identifying desperation in a fundraising conversation, and they price it accordingly. The booted strategy builds the alternative: a business with enough revenue and enough operating discipline to survive without external capital, which is precisely what creates the leverage to raise it well.

Bootstrapped vs VC-Backed vs Booted: A Practical Comparison

The table below compares the three main approaches across the dimensions that matter most to founders making capital strategy decisions.

| Dimension | Fully Bootstrapped | VC-Backed | Booted (Bootstrap-First) |

| Ownership at Series A | 100% | 55 to 70% | 80 to 90% |

| Capital Available (Y1) | Personal savings + revenue | 2M to 15M+ raised | Revenue + selective angels/grants |

| Growth Speed | Organic, revenue-paced | Aggressive, investor-paced | Moderate, milestone-paced |

| Decision-Making | Full founder control | Board and investor input | Primarily founder control |

| Failure Risk | Lower (lean by default) | Higher (burn rate pressure) | Low to moderate |

| Fundraising Leverage | Weak if approached early | Strong if thesis fits VC model | Strong (traction-backed) |

| Best For | Low-capital digital businesses | Capital-intensive, winner-take-all markets | Most SaaS, services, and niche tech startups |

| Exit Flexibility | High (no investor timeline) | Low (return expectations defined) | Moderate to high |

What the Founders Who Got This Right Actually Did

The companies most frequently cited as examples of successful bootstrapped or booted fundraising share a set of behaviours that are worth examining specifically, because the popular narrative around these companies tends to flatten them into simple origin stories.

Mailchimp did not simply avoid investors and get lucky. Ben Chestnut and Dan Kurzius ran a web design agency for years, used client revenue to fund the development of the email tool as a side project, and grew it to millions in annual recurring revenue before it ever became the headline business. By the time they were in a position to raise capital, they had a product with proven retention, a large customer base, and no need for external money, which is exactly why they never took it. They sold to Intuit in 2021 for twelve billion dollars with no venture capital dilution.

Zoho has been profitable and privately owned since its founding in 1996. Sridhar Vembu built the company through a combination of lean operations, long-term product development, and a deliberate decision to serve the SMB market that venture capital consistently undervalued because the deal sizes were not large enough to move the needle on a VC fund’s returns. The company now serves over 100 million users across more than 50 products. It has never taken outside investment.

Basecamp, founded by Jason Fried and David Heinemeier Hansson, is perhaps the most articulate example of the booted philosophy as a deliberate operating choice rather than a constraint. Both founders have written and spoken extensively about the relationship between capital structure and company culture. Their argument is that the pressure to grow fast and return capital to investors systematically distorts the decisions a company makes, and that building on revenue alone produces better products, healthier organisations, and more sustainable outcomes for everyone involved.

What these examples share is not the absence of ambition. It is the presence of clarity about what they were building, for whom, and on what terms. That clarity is what the booted fundraising strategy is ultimately designed to protect.

The Psychological Traps That Derail Booted Fundraising Strategies

The mechanics of the booted strategy are not especially complex. The psychology is harder. Founders pursuing this path face a set of cognitive and emotional traps that the startup funding culture makes worse, not better.

The Comparison Trap

Nothing undermines a bootstrapped founder’s confidence faster than reading about a competitor’s funding round. A competitor raising five million dollars at a 20-million-dollar valuation looks, from the outside, like an unambiguous victory. What it actually represents is the sale of 25 percent of that company for capital that may or may not be deployed effectively and that comes with return expectations that may or may not align with what the founder wants to build. The comparison is real, the implications are not straightforward, and founders who chase fundraising to keep up with competitors rather than to solve a specific strategic problem almost always regret it.

The Valuation Obsession

Founders who have bootstrapped through early growth sometimes arrive at fundraising conversations with an inflated sense of what their traction is worth, partly because they have worked extremely hard for it and partly because startup media celebrates high valuations as though they were achievements in themselves. A high valuation at the seed stage is only valuable if it reflects genuine market potential and if subsequent rounds can be raised at even higher valuations. A founder who raises a seed round at an aggressive valuation and then cannot grow into it faces a down round, which is psychologically crushing and practically damaging to future fundraising.

The Perfectionism Delay

Some founders use the logic of the booted strategy, wait until you have traction, as a justification for never starting the fundraising process at all. Every quarter there is a reason why the metrics are not quite right yet, why one more cohort of retention data would make the story cleaner, why the product needs one more feature before investors will take it seriously. This is not strategic patience. It is perfectionism dressed as strategy. The right time to raise is when the conditions described earlier in this guide are met, not when you feel completely ready.

The Identity Attachment to Non-Dilution

For some founders, bootstrapping becomes an identity rather than a strategy. Refusing external capital starts as a practical decision and gradually becomes a point of pride that prevents clear-eyed evaluation of when capital would actually serve the business. The goal of the booted strategy is to raise capital on good terms when you need it, not to avoid capital forever. Founders who confuse those two things sometimes allow competitive dynamics to outrun them while waiting for a fundraising moment that they have defined so narrowly it never arrives.

Mistakes That Cost Booted Founders Equity and Opportunity

- Raising capital before product-market fit is confirmed. The most expensive mistake in startup fundraising is selling equity before the business model is validated. Investor capital will not manufacture product-market fit. It will accelerate whatever is already happening, good or bad.

- Taking money from misaligned investors even at a good valuation. Capital from an investor who expects venture-scale returns from a business built for steady profitability is a structural conflict that will surface at every major decision point. Valuation is one dimension of a funding decision. Investor alignment is at least as important.

- Neglecting cap table hygiene from the beginning. Every SAFE, every convertible note, every advisor equity grant dilutes future rounds. Founders who are casual about early-stage equity documents often discover at Series A that their ownership has been diluted further than they expected. Model the dilution from every instrument before issuing it.

- Conflating revenue with product-market fit. Revenue is necessary evidence but not sufficient. Customers who churn quickly are paying you to try the product, not to keep it. Retention is the metric that distinguishes a business from a trial. Raise when retention is strong, not simply when revenue exists.

- Underestimating the time fundraising takes. A seed round from first outreach to capital in the bank typically takes three to six months. Founders who start the fundraising process when runway drops below three months are negotiating under duress. Start the process with at least six to nine months of runway remaining.

- Failing to use the bootstrapped phase to build investor relationships before you need them. The best fundraising conversations are those where the founder and investor have a relationship that predates the ask. Joining relevant communities, attending industry events, contributing publicly to your field, and meeting potential investors as a peer rather than a supplicant makes every subsequent conversation more efficient.

Frequently Asked Questions

Q1. What is a startup booted fundraising strategy?

A startup booted fundraising strategy is an approach where founders build meaningful traction using their own resources before seeking external capital. The core principle is that you raise money to accelerate growth that already exists rather than to create growth from scratch. This sequencing produces better fundraising terms, less dilution, and greater founder control than raising at the idea stage.

Q2. How is the booted fundraising strategy different from pure bootstrapping?

Pure bootstrapping means building an entire company without any external investment and often reflects a deliberate commitment to staying independent indefinitely. The booted fundraising strategy does not foreclose external capital. It changes when and how that capital enters the business. The goal is to use early bootstrapped growth to build the leverage that produces better fundraising outcomes, not to avoid fundraising entirely.

Q3. When should a bootstrapped startup start fundraising?

The right time to raise external capital is when three conditions are met: you have paying customers with measurable retention, your unit economics are sound with customer lifetime value exceeding acquisition cost, and you have identified a specific growth bottleneck that capital can remove and that organic revenue cannot fund quickly enough. Raising before these conditions are met typically results in higher dilution and less favourable terms.

Q4. What types of funding are available to bootstrapped startups?

Bootstrapped startups have access to angel investors, revenue-based financing, non-dilutive government grants through programmes like SBIR, startup accelerators, and SAFE-based angel rounds. Each of these sources suits different stages and business types. Revenue-based financing works best for recurring revenue businesses. Government grants work best for research and development-intensive companies. Angel investors provide capital alongside relationships and expertise.

Q5. Does bootstrapping hurt a startup’s valuation when it eventually fundraises?

In most cases it improves it significantly. Startups that arrive at fundraising conversations with revenue, customers, and operating history consistently raise at higher valuations and on better terms than those raising at the idea stage. Investors pay more for demonstrated traction than projected potential because demonstrated traction carries lower risk. The dilution from a seed round raised with strong metrics is typically far lower than the dilution from raising without them.

Q6. Which types of startups are best suited to the booted fundraising strategy?

The strategy works best for businesses where early revenue is achievable without significant capital expenditure. Software companies, SaaS businesses, professional services, consulting practices, content businesses, and digital marketplaces are well suited. Hardware, biotech, deep tech, and businesses requiring significant infrastructure investment before any revenue is possible may need external capital earlier and are less naturally suited to the booted approach.

Q7. What is revenue-based financing and how does it work for startups?

Revenue-based financing is a form of capital where an investor provides an upfront sum in exchange for a percentage of monthly revenue until a predetermined repayment cap is reached. It does not dilute equity and does not require fixed monthly payments regardless of revenue performance. It works best for businesses with recurring revenue and predictable retention. The cost of capital is higher than traditional debt but the terms are more flexible and ownership is preserved.

Q8. How do SBIR grants work and can most startups access them?

The Small Business Innovation Research programme distributes over three billion dollars annually to US small businesses conducting research and development. Phase one grants range from 50,000 to 275,000 dollars and require no equity and no repayment. Phase two grants can reach two million dollars. Eligibility requires the business to be US-based, for-profit, and primarily owned by US citizens. The application process is demanding, which keeps competition lower than the funding size would suggest.

Q9. What metrics do investors look for in a booted startup raising for the first time?

Investors evaluating a bootstrapped startup’s first external raise focus on monthly recurring revenue and its growth trajectory, net revenue retention showing whether customers expand their spending over time, customer acquisition cost relative to lifetime value, gross margins indicating scalability, and the founder’s explanation of specifically what the capital will do and why organic revenue cannot achieve the same result at the required speed.

Q10. Is the startup booted fundraising strategy viable in competitive markets?

It depends on the nature of the competition. In markets where execution quality, customer relationships, and product depth matter more than pure speed of distribution, the booted strategy is highly viable and often produces more durable competitive positions than those funded by large capital raises. In markets with genuine winner-take-all dynamics, strong network effects, or where first-mover advantage is structurally decisive, the need for capital speed may outweigh the benefits of the booted approach.

Conclusion

The startup booted fundraising strategy is ultimately a bet on sequencing. It is the belief that building real value before asking someone to fund that value produces better outcomes for founders, for companies, and in most cases for investors too.

The venture capital model is not broken, but it is not the right model for most startups in most markets. The companies that have demonstrated this most clearly are not obscure edge cases. They are Mailchimp and Zoho and Basecamp and hundreds of smaller businesses that their founders built patiently, on their own terms, without surrendering ownership before they understood what they were building.

The path is not glamorous. There are no press releases for the month you hit your first 10,000 dollars in monthly recurring revenue. There are no headlines when you turn down a term sheet because the terms were not right. The milestones of the booted strategy are internal ones: the unit economics that finally make sense, the retention curve that starts to flatten at the right level, the investor conversation where you can say genuinely and credibly that you do not need the money but you want the right partner.

That is the position the booted fundraising strategy is designed to produce. Not every founder will reach it. But the ones who do raise capital on terms that most founders who chase funding from the beginning never see.