You see the advertisement on a website, a social media post, or a roadside banner. The number looks genuinely good. Maybe better than you expected. You drive to the dealership feeling like you have already done your homework and know what you are walking into.

Then something happens between that advertised price and the figure on the contract in front of you. Fees appear. Add-ons get mentioned casually as though they were always part of the deal. A market adjustment shows up on the window sticker. By the time the finance manager slides the paperwork across the desk, the number is several thousand dollars more than what brought you through the door.

This is not an accident. It is not a misunderstanding. It is the result of a set of deliberate, well-practised dealership advertised pricing tactics that the automotive retail industry has refined over decades. Some of these tactics operate in legal grey areas. Some are entirely above board but deliberately confusing. And some, in certain states, cross the line into deceptive trade practices.

Understanding how these tactics work is not about assuming every dealership is dishonest. Many are not. It is about walking into one of the largest purchases most people ever make with the same level of information that the person on the other side of the desk has. This guide gives you that information, tactic by tactic, so that nothing in the showroom catches you unprepared.

Contents

- 1 What Are Dealership Advertised Pricing Tactics?

- 2 The Psychology Behind Why These Tactics Work So Well

- 3 Every Major Dealership Advertised Pricing Tactic Explained

- 4 Common Dealer Fees and What to Do About Each One

- 5 What the Law Actually Says About Dealership Advertised Pricing

- 6 How to Protect Yourself from Every One of These Tactics

- 7 Mistakes That Cost Car Buyers the Most Money

- 8 Frequently Asked Questions

- 9 Conclusion

What Are Dealership Advertised Pricing Tactics?

Dealership advertised pricing tactics are the methods car dealers use to present prices in advertising that attract buyers while preserving room to increase the actual transaction price during the sale. These tactics range from advertising prices that include conditional rebates most buyers do not qualify for, to omitting fees from the headline price, to adding on products after a price has been agreed upon. The gap between the advertised price and the final out-the-door price is where most of the dealership’s margin lives.

According to consumer research cited across multiple automotive publications, nearly 71 percent of all used car listings involve some form of pricing that does not reflect the true cost to the buyer. The Federal Trade Commission has taken action against misleading auto advertising practices, and multiple state attorneys general have issued specific rules about what dealers can and cannot include in advertised prices. Yet the tactics persist because they are effective, often technically legal, and because most buyers do not know what to look for.

The Psychology Behind Why These Tactics Work So Well

Before getting into the specific tactics, it is worth understanding why they are so consistently effective. The answer lies in a combination of cognitive psychology, information asymmetry, and the emotional state of someone who has already decided they want a specific vehicle.

The first principle at work is anchoring. When a buyer sees a price of $29,900 in an advertisement, that number becomes the mental reference point for the entire negotiation. Everything that happens afterward is evaluated relative to that anchor. Adding $2,000 in fees to a $29,900 advertised price feels less significant than if the advertised price had been $31,900 from the start, even though the buyer pays the same amount. Dealerships understand anchoring deeply and use it deliberately.

The second principle is commitment and consistency. Once a buyer has driven to a dealership, sat down with a salesperson, taken a test drive, and started completing paperwork, the psychological cost of walking away grows with each passing minute. The dealership has invested time in you and you have invested time in the process. Adding fees late in the transaction exploits this commitment. Most people will absorb several hundred dollars in additional charges rather than restart the entire process elsewhere.

The third principle is information asymmetry. The salesperson across the desk has negotiated hundreds of these transactions. They know exactly which fees are negotiable, which add-ons carry the highest margins, and how to present numbers in ways that obscure the total cost. Most buyers do this a handful of times in their lifetime. That gap in experience is enormously valuable to a dealership.

The fourth principle is emotional investment. By the time a buyer is sitting in the finance office, they have often already told their family they found the car. They have mentally imagined driving it home. That emotional investment makes it extremely difficult to walk away from a deal that has gone off course, which is precisely why so many of the most profitable tactics happen late in the process rather than upfront.

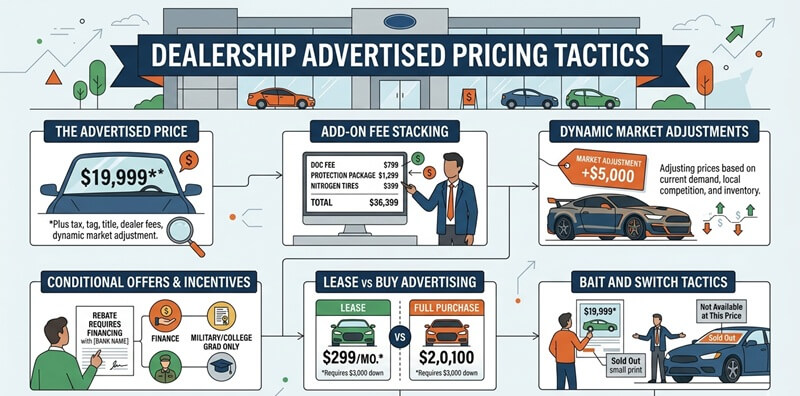

Every Major Dealership Advertised Pricing Tactic Explained

The Conditional Rebate Advertisement

This is one of the most widespread and least understood tactics in automotive advertising. A dealership advertises a vehicle at a price that looks genuinely competitive, sometimes several thousand dollars below what comparable listings show. What the advertisement does not say clearly is that this price is only available after stacking multiple rebates, most of which the average buyer does not qualify for.

These rebates might include a loyalty discount that requires you to already own the brand, a recent college graduate discount, a military service discount, a first responder discount, and a financing bonus that requires you to use the dealer’s financing at a specific rate. Each rebate is real and available to someone. But the probability that a given buyer qualifies for all of them is low, and the advertised price assumes they all apply.

The fine print says the price is after all applicable incentives, which is technically accurate but functionally misleading. The Federal Trade Commission’s guidelines on advertising require that material limitations on advertised prices be disclosed clearly and conspicuously. Many dealers satisfy this requirement with a block of text in eight-point font at the bottom of a web page or television advertisement that appears for four seconds.

What to do: Before driving to the dealership, call and ask specifically which rebates are included in the advertised price and which ones you personally qualify for. Get the eligible price confirmed in writing before you make an appointment.

The Bait and Switch

The bait and switch in its classic automotive form works like this. A dealer advertises a specific vehicle at an attractive price. When the buyer arrives, they are told that vehicle has just been sold, or it was the only one at that price, or it was a special fleet unit that is no longer available. They are then shown a similar vehicle at a higher price and encouraged to consider it instead.

In its more sophisticated modern form, the vehicle is technically still available but suddenly has mandatory add-ons that the salesperson presents as already installed and non-removable. Dealer-installed accessories like paint protection, nitrogen tyre fills, theft deterrent devices, and window tinting are presented as standard inclusions, effectively raising the price without changing the advertised figure.

This practice occupies a genuine legal grey area. Several states have specific rules requiring dealers to honour advertised prices. Texas law, for example, states that if a vehicle is advertised at a price, the dealer must be willing to sell it at that price. California law is similarly explicit. But enforcement varies significantly, and dealers in states with weaker consumer protection laws face fewer consequences.

What to do: Confirm via email before your visit that the specific vehicle you are interested in, identified by its VIN number, is available at the advertised price with no mandatory add-ons. This creates a paper trail that strengthens your position.

Monthly Payment Focus Instead of Total Price

This is perhaps the most profitable single tactic in the dealership playbook, and it works because most buyers make their budget decisions in terms of monthly affordability rather than total cost. A buyer who can afford $450 per month is not thinking about whether the total price is $28,000 or $35,000. They are thinking about whether $450 fits their monthly budget.

The salesperson uses this by keeping the conversation focused entirely on the monthly payment. They extend the loan term, they lower the down payment discussion, and they adjust the interest rate within a range they control, all while maintaining a payment figure the buyer finds acceptable. A buyer who walks in saying they want to stay under $450 a month can end up paying $7,000 more for the same vehicle than a buyer who negotiated the total price directly.

The mathematics of this are straightforward. Moving from a 60-month loan to a 72-month loan on a $30,000 vehicle at a 7 percent interest rate increases the total amount paid by approximately $1,800, while reducing the monthly payment by around $45. The dealership benefits from the extended loan period while the buyer feels they are getting a better deal.

What to do: Negotiate exclusively on the total out-the-door price. Refuse to discuss monthly payments until the total price is agreed. Tell the salesperson that you will handle financing separately and that you want to see the full price of the vehicle, all fees included, before anything else.

Dealer Add-ons Presented as Non-Negotiable

Walk into any dealership’s finance office and you will almost certainly encounter a menu of additional products presented with the same matter-of-fact tone as the vehicle price itself. Extended warranties, GAP insurance, paint protection packages, tyre and wheel coverage, key replacement programmes, and interior fabric treatment are presented on a printed sheet as though they are standard components of the transaction.

Some finance managers present these items as required by the lender. This is almost always false. The Consumer Financial Protection Bureau has clearly stated that optional add-on products cannot be presented as required for loan approval. If a finance manager tells you that the extended warranty or GAP insurance is required to get your financing approved, that is either misinformation or an illegal finance charge under federal law.

The margins on these products are substantial. A GAP insurance policy that costs the dealer $40 to $80 to acquire is routinely sold to buyers for $400 to $900. An extended warranty with a dealer cost of $400 to $600 is commonly sold for $1,500 to $3,500. These products are not inherently bad. Some buyers genuinely benefit from them. But they should be purchased after independent research, not at the point of peak emotional investment in a finance office.

What to do: Decline all add-ons in the finance office without exception. Tell the finance manager you will consider them separately after you have had time to compare options from other providers. If you want GAP insurance, your own auto insurer or credit union will almost always sell it for significantly less than the dealership price.

The Market Adjustment

During and after the pandemic inventory shortages, market adjustments became ubiquitous in new car sales. A market adjustment is a charge added to the MSRP for vehicles that are in high demand or short supply. It is the dealer’s way of capturing additional profit when buyers have limited alternatives.

Market adjustments typically appear as a second sticker on the vehicle window, separate from the manufacturer’s window sticker. They can range from a few hundred dollars on moderately popular models to tens of thousands of dollars on highly anticipated vehicles like new hybrid releases, limited-edition models, or vehicles with very long wait lists.

The market adjustment is technically legal. There is no law requiring a dealer to sell at MSRP. But it is worth knowing that MSRP stands for manufacturer’s suggested retail price, and the suggestion has historically been a ceiling, not a floor. A market adjustment inverts that entirely. Kelley Blue Book data from mid-2025 shows that new car transaction prices have normalised significantly from their pandemic peaks, which means market adjustments on standard models are increasingly unjustifiable and more negotiable than dealers suggest.

What to do: Research the current market transaction price for the specific model through Kelley Blue Book, Edmunds, or CarGurus before visiting any dealership. If the vehicle you want carries a significant market adjustment, contact multiple dealers across a wider geographic area. Even a 200-mile drive can save several thousand dollars on a high-demand model.

The Documentation Fee

Every dealership charges a documentation fee, sometimes called a doc fee or conveyance fee, to cover the administrative cost of processing the sale paperwork. The concept is legitimate. The execution varies enormously. Documentation fees in the United States range from under $100 in states with capped fees to nearly $999 in states with no regulatory limits.

Many buyers see the documentation fee listed on the contract and assume it is a fixed, government-mandated charge like a title fee or registration. It is not. It is a dealer charge, and in most states it is at least partially negotiable. Some states, including California, limit documentation fees to a specific maximum. Others, including Florida and Georgia, have no cap at all, allowing dealers to set whatever figure the market tolerates.

What to do: Research your state’s documentation fee rules before visiting a dealership. Know the typical range in your area and challenge fees that significantly exceed it. In the context of a total negotiation, a few hundred dollars on a doc fee is unlikely to derail a deal, but it is worth pushing back as part of an overall out-the-door price negotiation.

Advertising Fees Passed to the Consumer

Some dealerships include a line item on the purchase contract for an advertising fee, sometimes described as a regional advertising contribution or a dealer advertising assessment. This fee, typically ranging from $200 to $500, represents the dealer’s cost of participating in regional manufacturer advertising programmes.

This is unambiguously a cost of doing business for the dealership. It has no more legitimate claim to a place on a buyer’s invoice than the dealership’s electricity bill or the coffee machine in the waiting room. Several state attorney general offices have specifically identified advertising fees passed to consumers as deceptive when not disclosed in the advertised price.

What to do: Identify this line item early in the process and refuse it directly. Say clearly that you will not pay the dealer’s advertising costs and that if the fee cannot be removed, you will include it as part of your total price negotiation. Most dealers will either remove it or absorb it into a price concession elsewhere.

Online-Only Price Manipulation

A more recent tactic that has developed alongside the rise of online car shopping involves advertising prices on third-party platforms, like CarGurus, AutoTrader, and Cars.com, that are not fully honoured when the buyer arrives in person. The online price might require dealer-specific financing, a specific trade-in, or residency in a particular zip code. None of these conditions are clearly stated on the listing.

Alternatively, some dealers list vehicles online with attractive prices that exclude destination and delivery charges that are always applicable. When the buyer arrives, the actual vehicle price is several hundred dollars higher than listed before any negotiation begins. Third-party platforms have become increasingly aggressive about policing this behaviour, with CarGurus and others now flagging listings from dealers with patterns of price discrepancies. But the practice continues.

What to do: Screenshot the online listing, note the date and time, and confirm via email with the dealership that the price on the listing applies to you specifically with no additional conditions before making the trip. If the dealer cannot confirm this, treat the advertised price as unreliable.

Common Dealer Fees and What to Do About Each One

The table below covers the most frequently encountered fees and add-ons between the advertised price and the final out-the-door figure. Use this as a reference when reviewing any dealership’s purchase contract.

| Fee or Add-on | Typical Range | Negotiable? | What to Do |

| Destination / Freight Fee | $900 to $1,800 | No | Non-negotiable. Set by manufacturer. |

| Documentation Fee | $100 to $999 | Partially | Ask for a reduction. Varies by state law. |

| Dealer Preparation Fee | $200 to $600 | Yes | Push back. This is dealer profit. |

| Advertising Fee | $200 to $500 | Yes | Refuse it. It is the dealer’s cost, not yours. |

| Nitrogen Tyre Fill | $150 to $300 | Yes | Decline. Air works exactly as well. |

| Paint / Fabric Protection | $200 to $800 | Yes | Decline. Often already applied without consent. |

| VIN Etching | $100 to $400 | Yes | Decline or ask for it free. Costs a dealer almost nothing. |

| GAP Insurance | $400 to $900 | Yes | Buy from your own insurer for far less. |

| Extended Warranty | $1,000 to $3,500 | Yes | Shop separately. Never buy in the finance office. |

| Market Adjustment | $500 to $10,000+ | Negotiable | Walk away if inventory allows. It is pure margin. |

What the Law Actually Says About Dealership Advertised Pricing

The legal framework governing dealership advertised pricing is a patchwork of federal guidelines, state laws, and industry self-regulation. Understanding the broad outlines of this framework helps buyers know when they have genuine recourse and when a tactic, while frustrating, is technically within the rules.

At the federal level, the Federal Trade Commission Act prohibits unfair or deceptive acts in commerce. The FTC’s Used Motor Vehicle Trade Regulation Rule, commonly called the Used Car Rule, requires dealers to display a Buyers Guide on all used vehicles disclosing warranty terms. More broadly, the FTC has taken enforcement action against dealers whose advertising practices it deemed deceptive, including cases where advertised prices required conditions that were not clearly disclosed.

The FTC’s Combating Auto Retail Scams rule, known as the CARS rule, was proposed specifically to address advertising pricing deceptions and required dealers to disclose the full out-the-door price in all advertising. Its implementation has faced legal challenges, but it reflects the regulatory direction of travel in this area.

At the state level, the variation is significant. California’s Vehicle Code and the regulations of the California Department of Motor Vehicles are among the most consumer-protective in the country. California dealers are legally required to sell vehicles at or below the advertised price, and that advertised price includes any price shown on a third-party listing platform. Texas has similar requirements through its state DMV rules. Many other states have weaker protections, and some have virtually none beyond the general prohibition on fraudulent misrepresentation.

State attorneys general offices are generally the most effective route for reporting dealers who violate advertised pricing rules. The FTC also accepts complaints through its consumer reporting portal. It is worth knowing that individual legal action for a pricing violation is possible in many states, and several consumer protection attorneys work on contingency for auto fraud cases, meaning they take a fee from any recovery rather than charging upfront.

How to Protect Yourself from Every One of These Tactics

The good news is that knowledge is the most powerful tool available to a car buyer. Every tactic described in this article relies on information asymmetry. The moment you understand what the dealership is doing and why, the leverage shifts.

Do Your Homework on Price Before You Walk In

Research the market transaction price for the specific vehicle you want using Kelley Blue Book, Edmunds, and TrueCar. These platforms show what buyers in your area are actually paying, not just what dealers are asking. Know the invoice price, the typical dealer holdback amount, and any current manufacturer incentives that are broadly available. Walk in knowing what a fair deal looks like in numbers, not just in concept.

Get Pre-Approved for Financing Independently

Secure a pre-approval from your bank or credit union before visiting any dealership. This does two things. First, it gives you a financing baseline against which to compare the dealer’s offer. If the dealer can beat your rate, fine. If not, you have no obligation to use their financing. Second, it removes the monthly payment tactic from the conversation entirely. You know your rate, you know your loan term, and the only variable remaining is the total vehicle price.

Negotiate the Out-the-Door Price, Nothing Else

The out-the-door price is the total amount you will pay, including the vehicle price, all dealer fees, taxes, title, and registration. This is the only number that matters, and it is the only number you should negotiate. When a salesperson tries to discuss monthly payments, say clearly that you will discuss financing once the out-the-door price is agreed. Write the number down. Ask the salesperson to confirm it in writing before the finance office visit.

Identify and Challenge Each Fee Individually

When you review the purchase contract, go through every line item. Ask what each fee is for, who it goes to, and whether it is legally required. Fees for advertising, dealer preparation, nitrogen tyres, paint protection, and fabric treatment are all negotiable. Documentation fees vary by state but are often partially negotiable. Destination fees set by the manufacturer are not negotiable. Knowing the difference lets you focus your energy where it will have the most impact.

Be Genuinely Willing to Walk Away

The single most powerful tool a car buyer has is the credible willingness to leave. Dealerships know this. When a buyer has one foot out the door, prices become more flexible. When a buyer is clearly committed and emotionally invested, the opposite is true. Before entering any negotiation, identify at least two other vehicles at competing dealerships that meet your needs. This is not a bluff. It is a genuine alternative, and having one changes your posture in the entire conversation.

Use the Internet to Create Competition

Email five dealerships in your area with the same request. Tell them you are ready to buy the specific vehicle this week and that you are collecting offers. Ask each one for their best out-the-door price for the vehicle. This process does two things. It eliminates the high-pressure in-person environment from the initial price negotiation. And it creates genuine competition between dealers for your business, which consistently produces better outcomes than walking in cold to a single showroom.

Mistakes That Cost Car Buyers the Most Money

Even well-prepared buyers make predictable mistakes that the dealership’s sales process is specifically designed to encourage. These are the ones that consistently prove most expensive.

The first is telling the salesperson your budget or monthly payment limit upfront. The moment a dealer knows the most you are willing to pay per month, they will structure the deal to reach exactly that number while preserving maximum margin elsewhere. Never volunteer this information.

The second is trading in a vehicle at the same time as buying. Trade-in value and purchase price should be negotiated as entirely separate transactions. Dealers often use the trade-in to create the appearance of flexibility on the purchase price while actually reducing the trade-in value to compensate. Agree on the vehicle purchase price first, then introduce the trade-in discussion.

The third is making decisions in the finance office under time pressure. The finance office is where the most profitable upselling happens, and it happens after you have already spent hours at the dealership and are emotionally and physically exhausted. You have every right to take the contract home and review it overnight before signing. Any dealer who tells you the deal expires at the end of the day is applying pressure, not stating a fact.

The fourth is failing to check the final contract against what was verbally agreed. Numbers sometimes change between verbal agreement and the written contract. Read every line of the contract before signing. If a fee appears that was not discussed or agreed to, ask for it to be removed before proceeding.

The fifth is assuming that a certified pre-owned label means the price is fixed and fair. CPO vehicles carry a manufacturer-backed inspection and warranty, which is valuable. But the selling price of a CPO vehicle is no more fixed than any other used vehicle. The CPO designation covers the condition, not the price. Negotiate it the same way you would any other used car purchase.

Frequently Asked Questions

Q1. Why is the price at the dealership higher than the advertised price?

The advertised price typically excludes several categories of charges that appear later in the transaction. These include dealer fees like documentation and preparation charges, mandatory or dealer-installed add-ons, market adjustments on high-demand vehicles, and in some cases the advertised price reflects post-rebate pricing that requires qualifications most buyers do not meet. The gap between the advertised price and the final out-the-door price can range from a few hundred to several thousand dollars depending on the dealership and the vehicle.

Q2. Is a dealership legally required to honour its advertised price?

In many states, yes. California and Texas both have clear rules requiring dealers to sell vehicles at or below their advertised price. The Federal Trade Commission’s guidelines on deceptive advertising also apply at the federal level. However, enforcement varies significantly by state, and many dealer tactics, like advertising a price that requires multiple rebates the buyer may not qualify for, operate in grey areas that are technically compliant with the letter of the rules while being functionally misleading.

Q3. What is the out-the-door price and why does it matter?

The out-the-door price is the total amount you will pay to drive the vehicle away from the dealership. It includes the vehicle selling price, all dealer fees, taxes, title, and registration charges. It is the only number that gives you a complete picture of what a deal actually costs. Negotiating based on monthly payment or even vehicle price alone without knowing the out-the-door total leaves significant room for hidden costs to accumulate.

Q4. What dealer fees are negotiable?

Dealer preparation fees, advertising fees, nitrogen tyre fills, paint protection packages, fabric treatment, VIN etching, and extended warranty products are all negotiable or refusable. Documentation fees are partially negotiable in most states, though some states cap them by law. Destination and delivery fees set by the manufacturer are not negotiable. Government fees including sales tax, title, and registration are also non-negotiable as they are set by law.

Q5. What is a market adjustment and should I pay it?

A market adjustment is a charge added above the MSRP for vehicles that are in high demand or short supply. It is a way for dealers to capture additional profit when buyers have limited alternatives. Whether you should pay it depends on how urgently you need the vehicle and how difficult it is to find the same model elsewhere. As new car inventory has normalised from pandemic levels, market adjustments on most standard models are increasingly unjustifiable. Research availability at competing dealers before accepting one.

Q6. Is GAP insurance from the dealership worth buying?

GAP insurance itself can be valuable, particularly if you are financing more than 80 percent of a vehicle’s value or leasing. However, the dealer’s finance office is almost always the most expensive place to buy it. Dealers typically charge $400 to $900 for a product they acquire for $40 to $80. Your own auto insurer or credit union will almost always offer the same coverage for significantly less. Decline it at the dealership, then purchase it from your preferred provider within the first 30 days of ownership.

Q7. How do I negotiate an out-the-door price effectively?

Start by researching the fair market transaction price through Kelley Blue Book or Edmunds. Secure independent financing pre-approval so you are not dependent on dealer financing. Contact multiple dealers via email requesting their best out-the-door price for the specific vehicle you want. This creates competition without requiring an in-person visit. When you do visit, confirm the out-the-door price in writing before entering the finance office, and refuse add-ons individually as each one is presented.

Q8. Can a dealership refuse to sell me a car without add-ons?

A dealership can legally choose not to sell a vehicle without certain pre-installed features if those features are disclosed upfront and included in the advertised price. What it cannot legally do is present optional products as mandatory conditions of financing approval, as this constitutes an illegal finance charge under federal consumer protection law. If a dealer insists an add-on is required to obtain your loan, you can refuse and, if necessary, file a complaint with the Consumer Financial Protection Bureau.

Q9. What should I do if a dealer will not honour its advertised price?

First, confirm in writing the discrepancy between the advertised price and what you are being offered. Then, contact the dealership’s general manager directly, as many pricing disputes at the sales level can be resolved at a management level. If the dealer still refuses, you can file a complaint with your state attorney general’s consumer protection office, the Federal Trade Commission, or the Better Business Bureau. In states with strong consumer protection laws like California, you may also have civil remedies available through a consumer protection attorney.

Q10. What is the best way to avoid dealership pricing traps entirely?

The most effective approach is to do as much of the negotiation as possible before arriving at the dealership. Email multiple dealers requesting their best out-the-door price on the specific vehicle identified by model, trim, and if possible VIN number. Get the agreed price confirmed in writing before you visit. Arrive with pre-approved independent financing. Decline all add-ons in the finance office. Read the final contract carefully before signing. This process removes most of the high-pressure, in-person dynamics that these tactics depend on.

Conclusion

Dealership advertised pricing tactics are not going away. They are built into the economics of automotive retail, refined over decades, and effective enough that the industry has little incentive to abandon them voluntarily. Regulation is moving in the direction of greater transparency, but it moves slowly and unevenly across state lines.

What has changed significantly is the information available to buyers. A car buyer in 2025 with an hour of preparation and a clear understanding of what to look for walks into the dealership on far more equal terms than their counterpart twenty years ago. The tactics described in this article lose most of their power the moment a buyer can name them out loud and explain why they are declining them.

The advertised price is the beginning of a conversation, not the end of one. The out-the-door price is the only number that matters. Every fee, add-on, and adjustment between those two figures is negotiable, refusable, or at minimum worth understanding before you sign anything. That knowledge is the most valuable thing you can bring into any dealership.